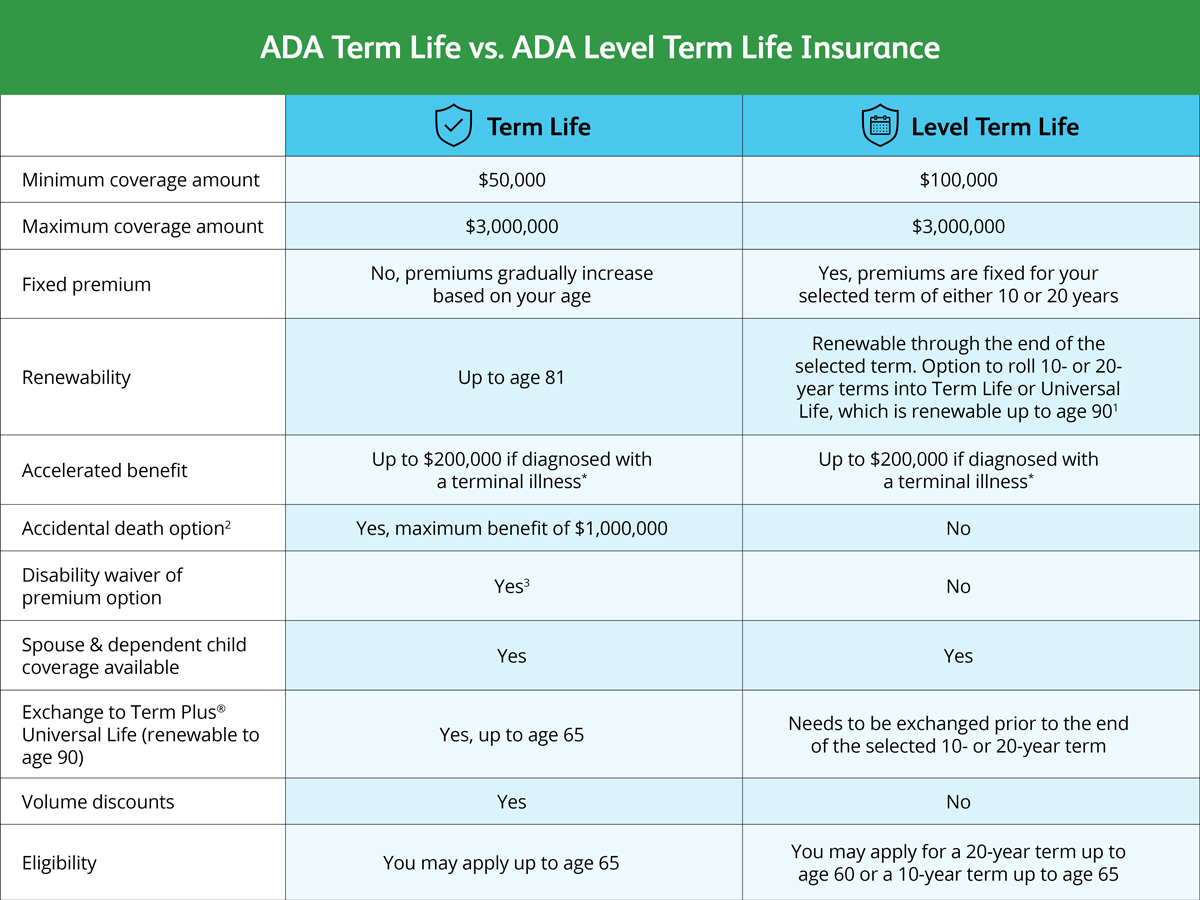

Understanding Term Life Insurance: Key Benefits and Features

Understanding term life insurance is essential for anyone considering financial protection for their loved ones. Unlike whole life insurance, which provides coverage for the policyholder's entire lifetime, term life insurance offers coverage for a specified period, typically ranging from 10 to 30 years. This makes it an attractive option for individuals seeking affordable premiums while ensuring that their dependents are financially secure during critical life stages, such as raising children or paying off a mortgage.

One of the key benefits of term life insurance is its affordability. Since it does not build cash value like permanent insurance, premiums are generally lower, allowing policyholders to secure a substantial amount of coverage without breaking the bank. Additionally, many policies offer flexible options, such as converting to permanent insurance as your needs change. In summary, term life insurance is a straightforward solution for providing temporary financial support and peace of mind during your most vital years.

Is Term Life Insurance Right for You? Common Questions Answered

When considering whether term life insurance is right for you, it's essential to evaluate your current financial situation and future needs. Term life insurance provides protection for a specified period, typically ranging from 10 to 30 years. This type of policy can be a viable option if you are looking for affordable coverage to secure your family's financial future in the event of an untimely death. It is particularly beneficial for those with temporary financial obligations, such as raising children or paying off a mortgage.

Before making a decision, you might have several questions about term life insurance. Common queries include:

- What happens when the term ends?

- Can I convert my term policy to a permanent one?

- How much coverage do I really need?

How to Choose the Right Term Length for Your Life Insurance Policy

Choosing the right term length for your life insurance policy is essential for ensuring that your coverage meets your financial needs. Typically, term lengths range from 10 to 30 years, and the ideal choice often depends on your individual circumstances, such as age, financial obligations, and personal goals. For instance, if you are a young parent with a mortgage and children to support, a longer term, such as 20 or 30 years, may provide the peace of mind you need. On the other hand, if you are nearing retirement with fewer financial responsibilities, a shorter term may suffice.

When evaluating your options, consider the following factors:

- Current Expenses: Assess your current financial obligations, including debts, mortgages, and your children's education costs.

- Future Goals: Think about any major life events you anticipate, such as retirement or college for your kids.

- Budget: Determine how much you can afford in premiums, as longer terms generally mean higher costs.